Robert Bouquet

The Natural Color Diamond Association (NCDIA) has published the latest comments from industry expert Robert Bouquet who reports on the diamond market for the organization. Bouquet says the global diamond market is showing the the first signs of a recovery.

Green Shoots Are Apparent; Now Is The Time For A Cautious And Sustained Recovery

After such a challenging and stressful last six months for the diamond industry, the first signs of a recovery in the diamond market are now in evidence and the industry is breathing its first collective sigh of relief. It was always going to happen eventually, and yet, despite the improvement in sentiment and activity, the huge uncertainty of what comes next remains.

Now what is required is a gentle hand on the tiller to ensure that we do not overshoot on the resumption of trade. The volume and pricing tactics of the two majors will be critical; their strategy over the last six months has worked, albeit at a significant cost to them both in terms of financial performance.

De Beers has announced its sales results for the last two sights ($116m and $320m, respectively) - better than many had predicted. Dropping prices in the 4 grainers and up had the desired effect and caught a positive tailwind driven by a combination of reduced cutting center stocks, factories reopening in India and increased demand for polished in advance of the key festive season.

Alrosa also dropped its prices and saw an improvement in sales. The Antwerp diamond district is noticeably busier, and tenders are better attended. Prices achieved at various tender and auction events have recovered to around 5% below pre-Covid levels.

Copyright: Petra Diamonds Ltd; five exceptional type IIb blue stones recovered in one week.

Large stone and fancy colour recoveries continue to make the headlines, with Gem Diamonds discovering several 100ct+ type IIa gems and Petra Diamonds unearthing five exceptional type IIb blue stones ranging from 9 carats to 25 carats from the historic Cullinan Mine in South Africa (all within one week!).

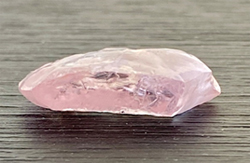

One tender house, Hennig Tenders, offered for sale in September a 45-carat exceptional pink stone along with a selection of 18 other pinks above 5 carats, all from Angola.

Junior miners who struggled even before the pandemic see an opportunity now to try to revive themselves. An example is Stornoway with its Renard mine in Quebec, Canada. Refinanced and reopening it will recommence production, as well as sell a 300kct stock it accumulated previously. Other juniors are trying to refinance and emerge from the ashes. The situation remains fragile and several mines were struggling pre-pandemic. Therefore, I do not foresee a sudden dramatic improvement in their fates, but they may survive given the right market movements.

Copyright: I Hennig & Co Ltd; 45 carat pink stone from Angola.

The imminent closure of Argyle mine in Australia will help the market, yet it is too early to say that a new equilibrium has been formed.

And so, the market for rough right now is strong as manufacturing in India is back to 70% capacity, orders for polished need to be filled and gaps in the supply in better goods are evident. The middle market has had an injection of profitability and is back in action. The Diwali break in manufacturing in India will be reduced to 10 days this year to capitalise on the polished demand and shortages of stock. Miners are also looking creatively at alternative ways to show their productions to the trade in various cutting centres as travel restrictions persist.

If the industry benefits from a strong retail festive season, the recovery could well be sustained into 2021, which would be very welcome to the trade - but of course, it remains a careful balancing act as the rough market does tend to overheat. Sensible pricing and volume by the majors combined with sensible buying by the middle market is required. We shall see what happens in the coming months.

Polished and retail

On the polished front, prices have firmed due to lack of availability after such reduced manufacturing activity. Demand is back and a positive sentiment prevails. Well-made goods, especially fancy shapes, seem to be the order of the day. Hard to move, slow-moving poorly made articles remain out of favour and can only be sold at larger discounts, if at all.

Rio Tinto has begun its annual Argyle tender of special pinks, with its headline stone a 2.24ct fancy-vivid-purplish-pink round, named by the miner Argyle Eternity. Bidding is expected to be fierce for these small but exceptional stones, as this is the penultimate sale as the mine draws to a close. Once the mine has been shuttered at year-end, a final sale of the very last exceptional Argyle pink polished is scheduled for 2021.

Copyright: Rio Tinto Diamonds; the “hero” stones of the Argyle Pink Tender 2020

GIA recently announced a review of its Antwerp operation and will either scale back significantly or close the whole operation. An announcement is expected soon.

Auction houses are embracing digital sales events in this new era, with Sotheby’s now holding weekly online sales.

Tiffany and LVMH are locked in a legal battle as LVMH attempts to exit its planned acquisition of the iconic US jewellery brand.

Diamond jewellery retail appears to be back on track as sales in mainland China strengthen and US retailers report better than expected results. The shift to online sales is clearly going to continue as buying habits evolve.

So, a good key season (Thanksgiving and Christmas in the US, followed by Chinese New Year) would be just the tonic for the industry and give us the ideal launchpad into 2021. Cautious optimism prevails; we know we are not out of the woods yet, but the green shoots of recovery are there.

The industry remains resilient and will prove itself once again. Once this pandemic is truly over, normality will return, and much happier times await. Demand for diamonds will endure as the ultimate symbol of love.